Russia-Ukraine conflict spurs Europe's FSRU drive

In the aftermath of the Russia-Ukraine conflict, piped gas supplies from Russia to Europe plunged last year. To reduce its dependency on Russian gas, Europe has raised LNG imports, with many of the cargoes diverted from Asia. The average regasification capacity utilization in Europe reached over 70% last year, compared to less than 50% in 2021. To increase LNG import capacity, a plethora of LNG terminal construction projects have been proposed in European countries from last year, with new schemes joined by some shelved projects being revived. These plans will become a key driver in global regasification capacity growth. Most of the planned terminals will be floating storage and regasification unit (FSRU) based, due to the shorter timelines of construction and flexibility in deployment of this type of technology. In the short term, new import capacities will solve bottlenecks in Western Europe to allow for more imports, but in the long term, and especially after the mid-2030s, Europe’s LNG demand will trend lower on account of energy transition goals on the continent. This will lead to reduced utilization of Europe’s regasification facilities and raise concerns about investment returns on the assets and long-term overcapacity.

Booming regasification construction in Europe

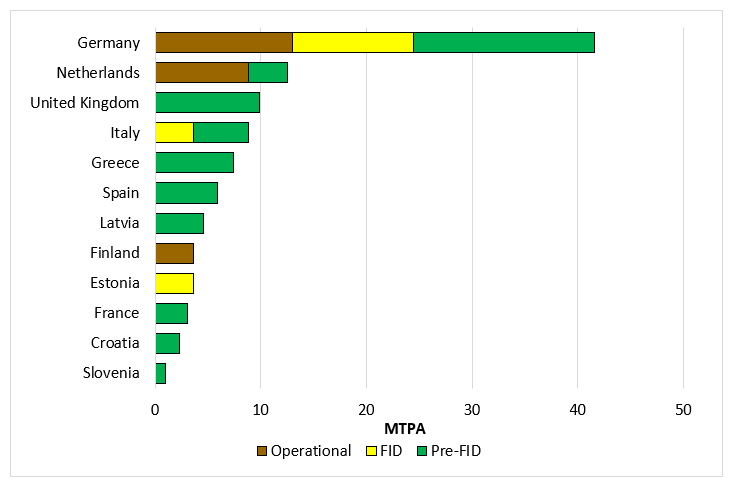

More than 10 European countries – among them Germany, the Netherlands, Finland, France, Croatia and Italy – have initiated regasification project construction plans since the Russia-Ukraine conflict broke out. This includes 26 projects with a combined regasification capacity of 104.5 million tonnes per annum (Mtpa). Nearly 70% of the new capacity will come from floating terminals, which can be brought online earlier and faster than onshore terminals. Of these projects, six have been commissioned, adding 25.5 Mtpa to global capacity as of April 2023, with another four under construction with total capacity of 18.8 Mtpa. With European countries’ efforts to expedite construction, it took just a few months last year to bring online the 5.9-Mtpa Eemshaven FSRU in the Netherlands and the 5.5-Mtpa Wilhelmshaven FSRU in Germany.

Figure 1: Europe regasification plans proposed since 2022, by status and market

Source: Rystad Energy LNG Solution

Last year, Germany was the first European country to announce plans to fast-track regasification construction. As the largest gas-consuming country in Europe, Germany had no LNG import terminals before 2022, relying instead on steady pipeline flows from Russia. The country has plans to add the highest amount of regasification capacity among European markets, at a projected 41.54 Mtpa. This involves building terminals at four sites – namely Wilhelmshaven, Lubmin, Brunsbuettel and Stade – each with two-phase construction and with start-ups between 2022 and 2026. Germany’s regasification capacity is expected to meet over 60% of its gas demand once all terminals start operating. Since December 2022, three projects with combined capacity of 13 Mtpa have been commissioned. German energy firm Uniper launched the country’s first LNG terminal, Wilhelmshaven FSRU Phase 1 with regasification capacity of 5.5 Mtpa, in mid-December last year, following the arrival of the FSRU Hoegh Esperanza. The 3.8-Mtpa Lubmin FSRU Phase 1, owned by private company Deutsche Regas, started operating in January 2023 after the arrival of the Neptune FSRU. The 3.7-Mtpa Brunsbuettel LNG terminal 1, owned by Germany utility RWE, received its commissioning cargo in February 2023, following the arrival of the FSRU Hoegh Gannet in January.

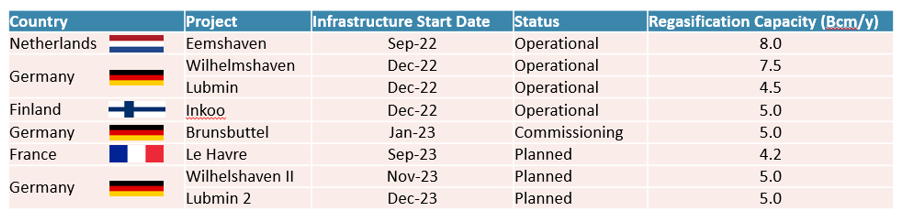

Figure 2: Upcoming regasification capacity buildout in Northwest Europe (2022-2023)

Source: Rystad Energy LNG Solution

Terminal buildout to resolve Western Europe's import capacity bottleneck

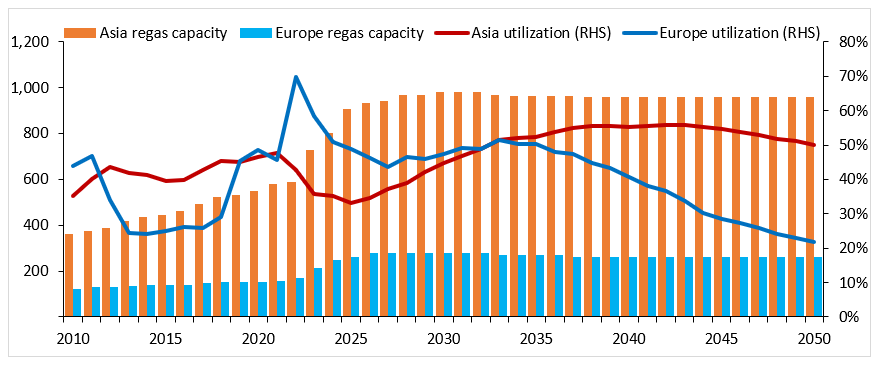

Asia and Europe will be the main drivers of global regasification capacity buildout, with capacity additions of 390 Mtpa and 110 Mtpa, respectively, between 2022 and 2030, accounting for over 70% and nearly 20%, respectively, of global capacity addition in the period. Some 56% of Europe’s LNG import capacity growth will come from Western Europe, which is the main gas-consumption hub in the region. Regasification utilizations have varied across sub-regions in Europe, with Western Europe witnessing notable capacity bottlenecks. Western Europe’s average regasification utilization in 2022 was as high as 76%, compared with 59% in Southern Europe. France and Belgium even witnessed utilization rates above 100%, given reloading and trans-shipment services in the countries’ terminals. Import capacity buildout can help to resolve the bottleneck in Western Europe to help capacity more closely match demand within each sub-region.

Germany has become a new LNG import market and imported over 1 million tonnes of LNG, since the commissioning of its first LNG terminal last December. The country now has more gas supply options other than the regional supplies and piped gas it had in the past, which can help Germany hedge its supply disruption risk. The Netherlands has been running its Gate LNG terminal at near full capacity with about 1 million tonnes of LNG inflows each month. With the start-up of Eemshaven FSRU from last September, the country’s monthly LNG imports could increase nearly 50% to 1.5 million tonnes. It is worth noting that Europe’s regasification utilization in 2023 is expected to fall below 60% as capacity rises faster than the region’s LNG demand.

Europe's long-term LNG demand to trend lower, weighing on investment perspectives for LNG terminals

Although many European countries have announced plans to build new terminals or revive old proposals, LNG demand in Europe is expected to fall back in the long term after peaking in the early 2030s. This may weigh on the prospect of promoting LNG projects in the region. With capacity additions outpacing the region’s LNG demand growth, Europe’s regasification utilization is expected to retreat below 50% by 2030 and drop further between 2030 and 2050 – in fact, utilization by 2050 is forecast to be only slightly above 20%. This raises concerns about potential over-investment in LNG terminals in Europe and about investment returns on such assets. This is another reason why European countries prefer FSRU-based terminals, supported by the flexibility of deployment and decommissioning. The fixed investment for floating terminals is also much lower than for onshore terminal. Asia’s utilization, meanwhile, will be largely flat, ranging between 45% and 55% from 2030 to 2050, as the largest long-term opportunity for gas demand is in Asia, which is on a slower pace of energy transition compared with Europe.

Unlike Asian countries, which have tended to secure LNG sources via term contracts, the share of contractual volumes in Europe’s LNG imports is still relatively low. This is a reflection on Europe’s push to increase energy security in the short-to-medium term as it presses ahead with its energy transitions plans. Current expectations are that most European countries are willing to pay higher prices for gas and provide support for gas infrastructure. While governmental support would make it easier to get projects off the ground, there are still hurdles along the way, such as the downward trend of the region’s gas demand in the long term and opposition from environmental groups. These factors made it more difficult to promote LNG projects before the Russia-Ukraine conflict – Germany’s Wilhelmshaven LNG was once cancelled in 2021, likely due to investors’ concerns over a lack of demand, while Vopak previously pulled out of Germany’s Brunsbuettel LNG project for similar reasons. Lower regasification utilization may also weigh on investors’ confidence over deploying import facilities, which could potentially cause delays to or cancellations of regasification projects. Tight supply of FSRU vessels could be another reason for delays or cancellations – construction works at Estonia’s Paldiski LNG terminal were completed in last October, but it has yet to secure an FSRU vessel to start operation. Finland and Estonia agreed to place the FSRU they chartered in Inkoo, Finland.

Figure 3: Regasification capacity and utilization in Asia and Europe 2010-2050

Source: Rystad Energy LNG Solution