Trading Signals & Macro Trends

Exclusive insights - Stay ahead of the market

Crafted by experts

Receive weekly oil trading insights

We publish a wide range of trading insights each week for our clients. This is your chance to receive a curated sneak peek.

Delivered straight to your inbox, our signals draw on high-frequency, short-term data. They cover oil supply, demand, real-time consumption, downstream refining and OPEC+ decisions.

Stay ahead of market shifts. Subscribe today.

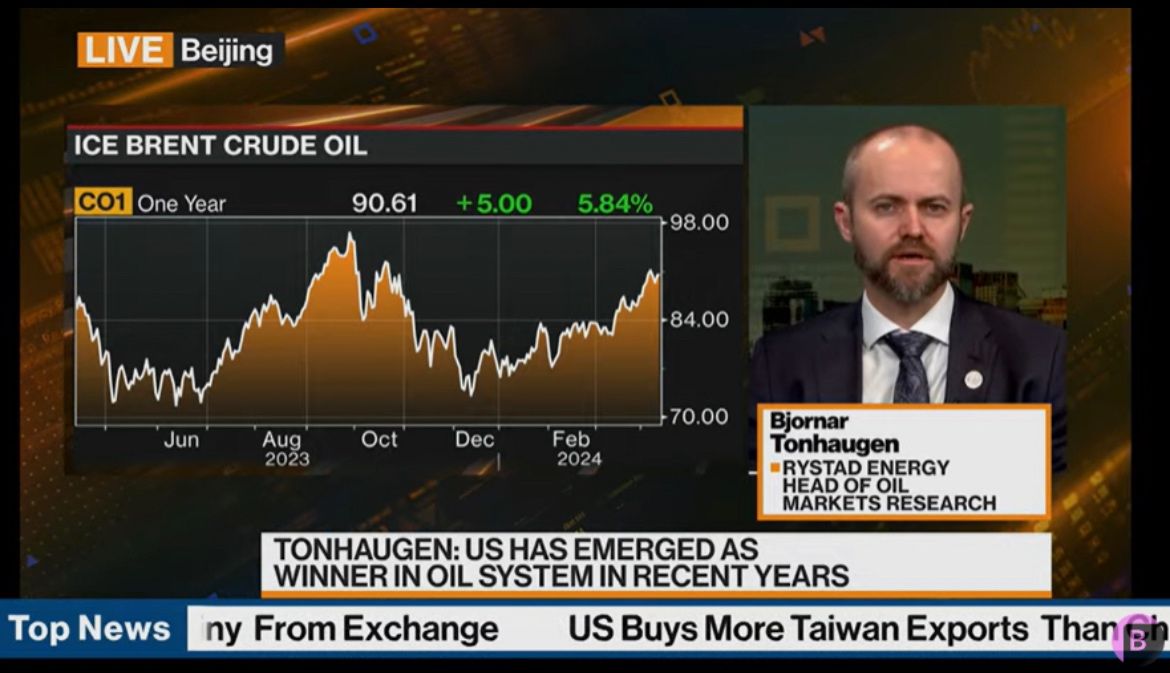

Features in the media

Loading form...